C both I and II. A material error would change the opinion of the average prudent investor.

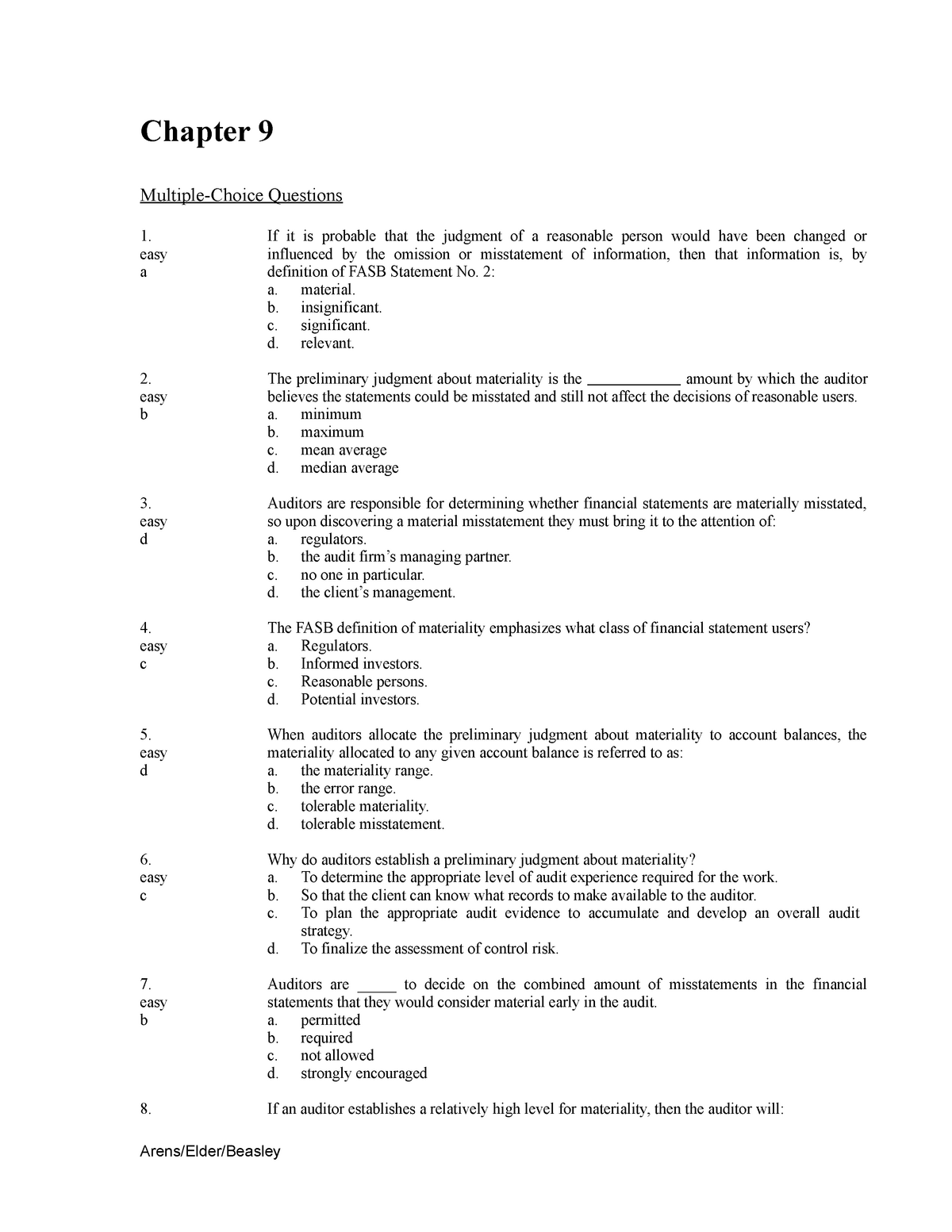

Chapter 09 Chapter 9 Materiality Multiple Choice Questions Chapter 9 Multiple Choice Questions Studocu

Auditors consideration of materiality is influenced by the auditors perception of the needs of an informed decision maker who will rely on the f d.

. If performance materiality is set too low the auditor might not perform sufficient procedures to detect material misstatements in the financial statements. Material misstatements should not exist in order for a company to receive an. Auditing is a type of attest service.

2 Which of the following is a correct statement. Which of the following statements about the materiality concept is not true. Which of the following statements about performance materiality is NOT true.

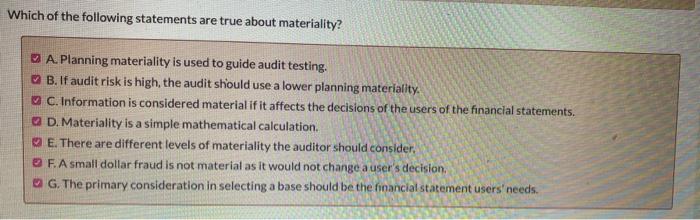

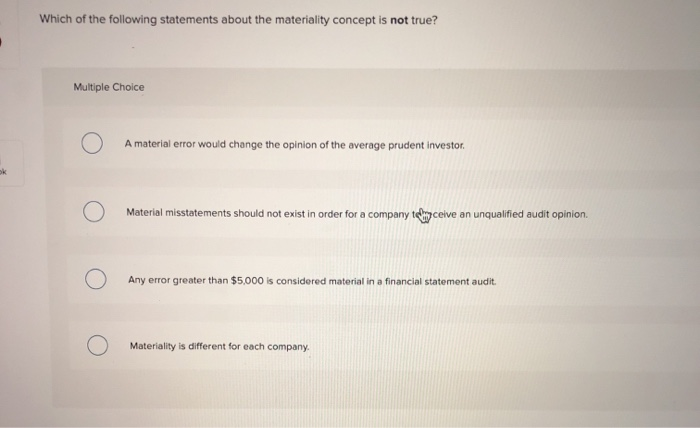

A material error would change the opinion of the average prudent investor. B Risk is a measure of magnitude or size. Material misstatements should not exist in order for a company to receive an.

D the sum of all the performance materiality levels can not exceed the preliminary judgment about materiality. Auditing services and attestation services are the same. Performance materiality is essentially the same as overall materiality.

Statements regarding preliminary materiality are true. Conflicts of interest often occur between absentee owners and managers. Any error greater than 5000 is considered material in a financial statement audit.

Preliminary materiality may change during the engagement. A There is no relationship between materiality and risk in auditing. If performance materiality is set too high the auditor might perform more substantive.

C The combination of performance materiality and the audit risk model factors determines planned audit evidence. February 03 2022. Materiality at the financial statement level is set at a higher level than planning materiality.

Materiality is different for each company. Any error greater than 5000 is considered material in a financial statement audit. In accounting materiality refers to the impact of an omission or misstatement of information in a companys financial statements on the user of those statements.

C professional judgment is critical. The concept of materiality recognizes that some matters are important for fair presentation of financial statements in conformity with GAAP while other matters are not important. If performance materiality is set too ow the auditor might not perform sufficient procedures to detect material misstatements in the financial statements.

D neither are true. B II only. An auditors consideration of materiality is influenced by the auditors perception of the needs of a reasonable person who will rely on the financial statements.

Multiple Choice Materiality is different for each company. The risk that auditors will not be able to complete the audit on a timely basis. All of the following are true except.

A materiality level where. If it is probable that users of the financial statements would have altered their actions if the information had not been omitted or misstated then the item is considered to be. D Performance materiality is part of the audit risk model.

B Performance materiality refers to the amounts set by the auditor at higher than the. Decision makers demand reliable information that is provided by accountants. At the planning state the auditor considers materiality at the financial statement level only.

The probability that a material misstatement could occur and not be detected by auditors procedures. Information asymmetry seldom occurs. Performance materiality is set less than overall materiality and helps the auditor determine the extent of audit evidence to obtain.

The probability that a material misstatement could not be prevented or detected by the entitys internal control policies and procedures. A I only. Which of the following statements about materiality is not true.

A Performance materiality is used to reduce the risk that the aggregate of uncorrected and undetected misstatements exceeds materiality for the financial statements as a whole to an acceptable level. Preliminary materiality is the maximum amount by which the auditor believes the financials. B only overstatements need to be considered.

If performance materiality is set too high the auditor might perform more substantive procedures than necessary. A it is easy to predict in advance which accounts are most likely to be misstated. Planning materiality moves in the same direction as tolerable misstatement.

Could be misstated and still not affect the decisions of reasonable users.

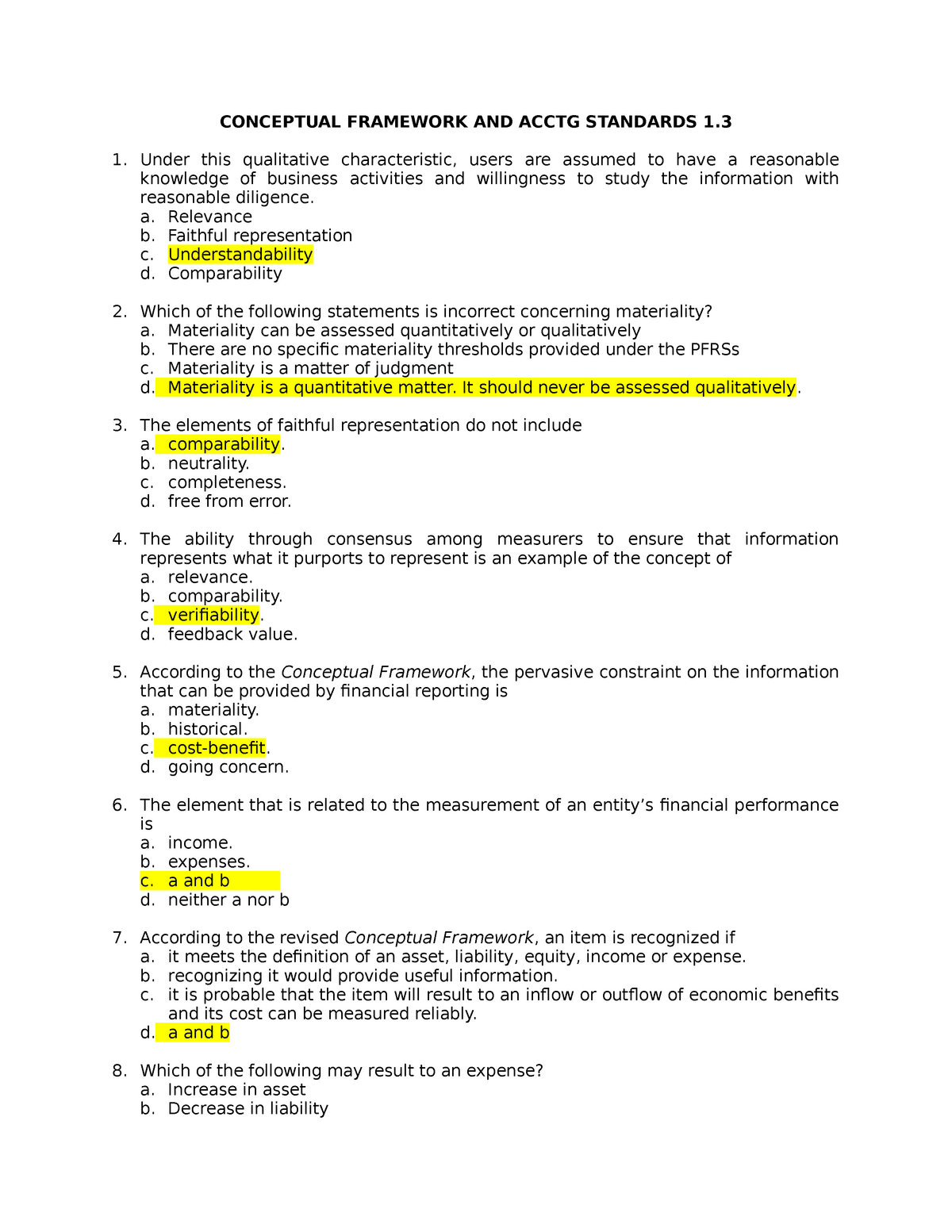

Conceptual Framework And Acctg Standards 1 3 Under This Qualitative Characteristic Users Are Studocu

Solved Materiality Is An Important Aspect Of Any Audit Chegg Com

Solved Which Of The Following Statements About The Chegg Com

0 Comments